Risk

Claims Experience Risk Factors for Employee Benefits

Feb 01, 2023

Risk

When it comes to investments, we’re constantly reminded that past performance is no indication of future growth, but this isn’t the case for group risk products. An organisation’s claims experience can be a valuable indicator of how its cover will perform in the future.

When an insurer prices a group risk scheme, it will factor in how the scheme has performed by looking at the claims history over the past five years. Where it’s the incumbent insurer, it will hold this information or it will request this when it’s quoting for a new piece of business.

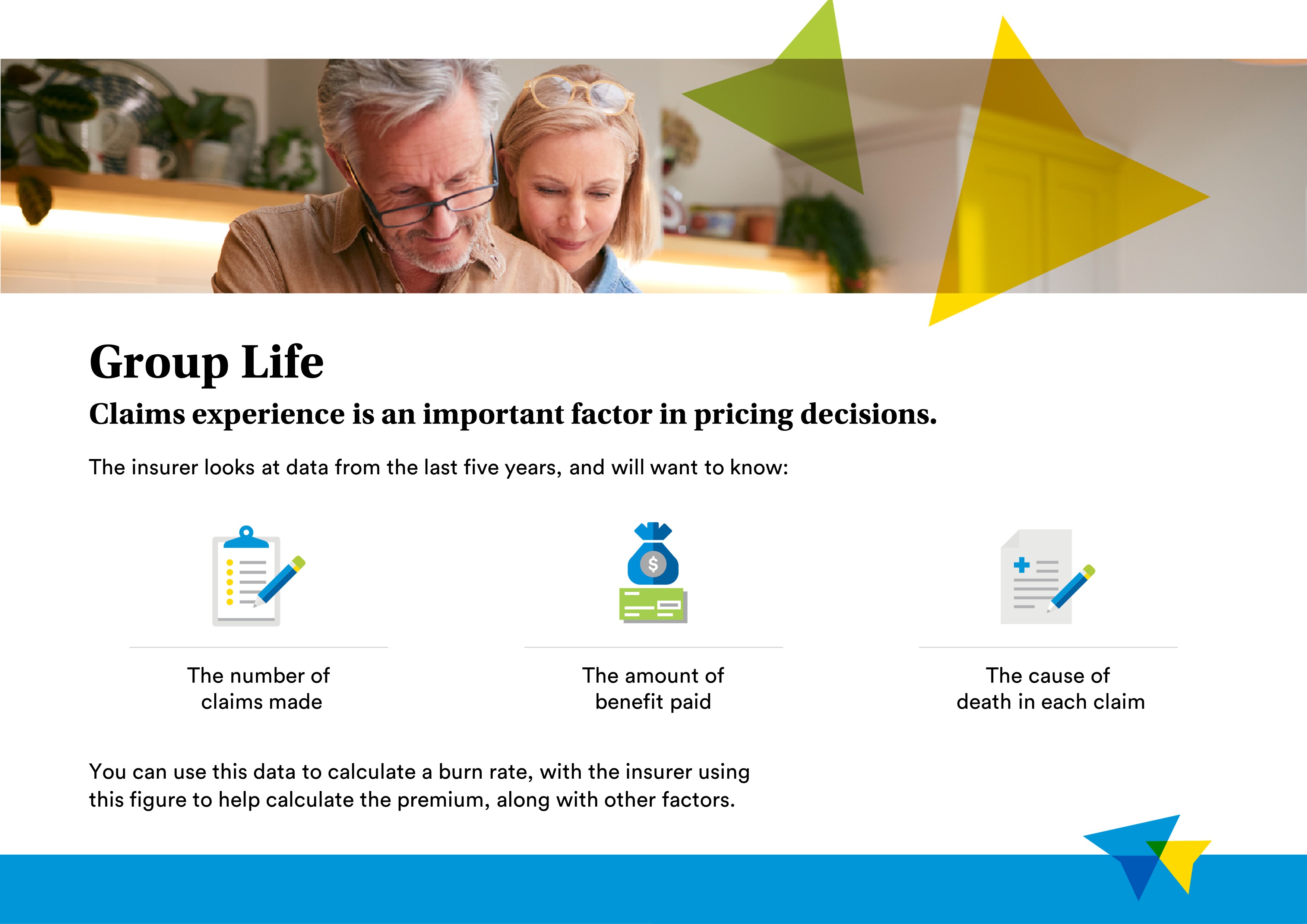

This is the simplest of the group risk products when it comes to the claims experience that is required and how it is applied to a quotation. An insurer will want to know the number of claims made, the amount of benefit paid and the cause of death in each claim over the past five years.

Calculating a burn rate can provide some insight into future pricing. This is the annual rate the insurer would have had to charge to cover the cost of claims.

The rate is calculated by dividing the total claim amount for the scheme year by the total policy benefit. This figure is then multiplied by 1,000 to get a rate per £1,000 of sum assured.

How much weight an insurer will give to this figure as an indicator of future performance varies. The scheme needs to be large enough, typically 1,000 members plus, for it to provide a reasonable indication of future claims. On a smaller scheme, the figures can be distorted by a year with additional claims: on a large scheme, this volatility is more likely to be smoothed out.

A group life insurer will also look at whether there is adequate claims experience and stability to give the burn rate credibility. Looking at the cause of death can help too, providing insight into whether the pattern may be repeated going forward.

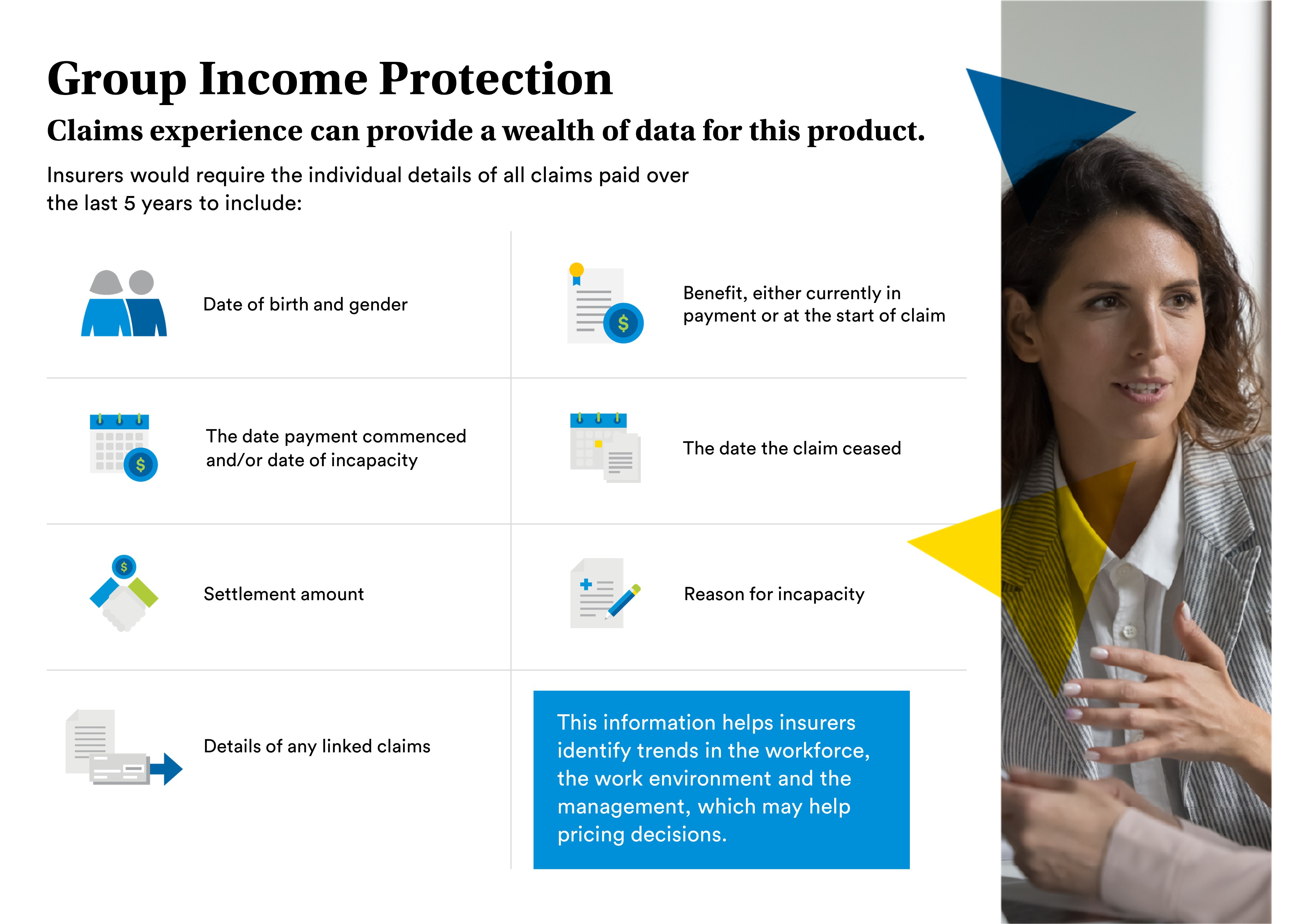

On group income protection, the information required is more detailed but it can also provide greater insight into how the scheme is likely to perform going forward.

The claims information required includes the member’s date of birth, gender and location; the cause and length of the claim; and, if a claim has ceased, the reason it was settled.

Interpreting this information is more complex than with group life and an insurer will look to identify any trends. For example, the data may show there are a high number of claims for stress coming out of one location. Is it the nature of the job, or something particular to that location, such as poor management, high performance targets or even a culture of going off with stress?

Insurers will also look for more detail where an organisation is seeing higher than average claims for musculoskeletal conditions. This may be down to the nature of the work or it could be linked to the level of support or training provided by the employer.

Evidence that the employer is addressing these conditions, whether through training, improved working conditions or early access to support and treatment, could result in fewer of these claims going forward.

The cause of claims is also significant. The top cause of group income protection claims is cancer but this is much less of an issue from a group income protection insurer’s perspective than two of the other major causes of claims – mental illness and musculoskeletal problems.

Most cancer claims are unlikely to result in a lengthy claim, with members either responding well to treatment and returning to work or sadly passing away. Conversely, the nature of mental illness and musculoskeletal problems makes these conditions more difficult to treat, with claims potentially long-term, especially where appropriate treatment isn’t accessed early.

The length of claims will also make a difference to insurers. The longer someone is off work, the smaller their chances of a return become. While some long-term claims are unavoidable, a proactive approach to rehabilitation and helping employees return to work can cut the average length of claims, especially for musculoskeletal problems and mental illness.

The type of policy will determine how much of an issue this is for the insurer. On a limited term policy, there is a cap on the size of the claim the insurer will pay but it is still beneficial for an organisation to look at how it can reduce these types of claim.

Group income protection insurers will also look at any ceased claims, taking into consideration the cause of the claim and why it was settled. Some claims will naturally be short, for example a broken leg may prevent someone from returning to a physically active role for six months. For other claims, the insurer will look at whether it was shortened as a result of the support the member received to get back to work.

Claims experience is a valuable tool for insurers, advisers and their clients. As well as helping to set an appropriate price for each risk, it can highlight areas for improvement in an organisation’s approach to employee health and wellbeing.