Technical

Extensions to cover

Feb 19, 2022

Technical

Greater flexibility around work coupled with life events such as becoming a parent, taking a sabbatical or long-term illness mean that Group Risk cover needs to be able to adapt to modern working practices.

To ensure employees benefit from continuity of cover in these circumstances, insurers offer a variety of extensions of cover.

This video explores all four extensions of cover typically offered in Group Risk, and explains simply how they work.

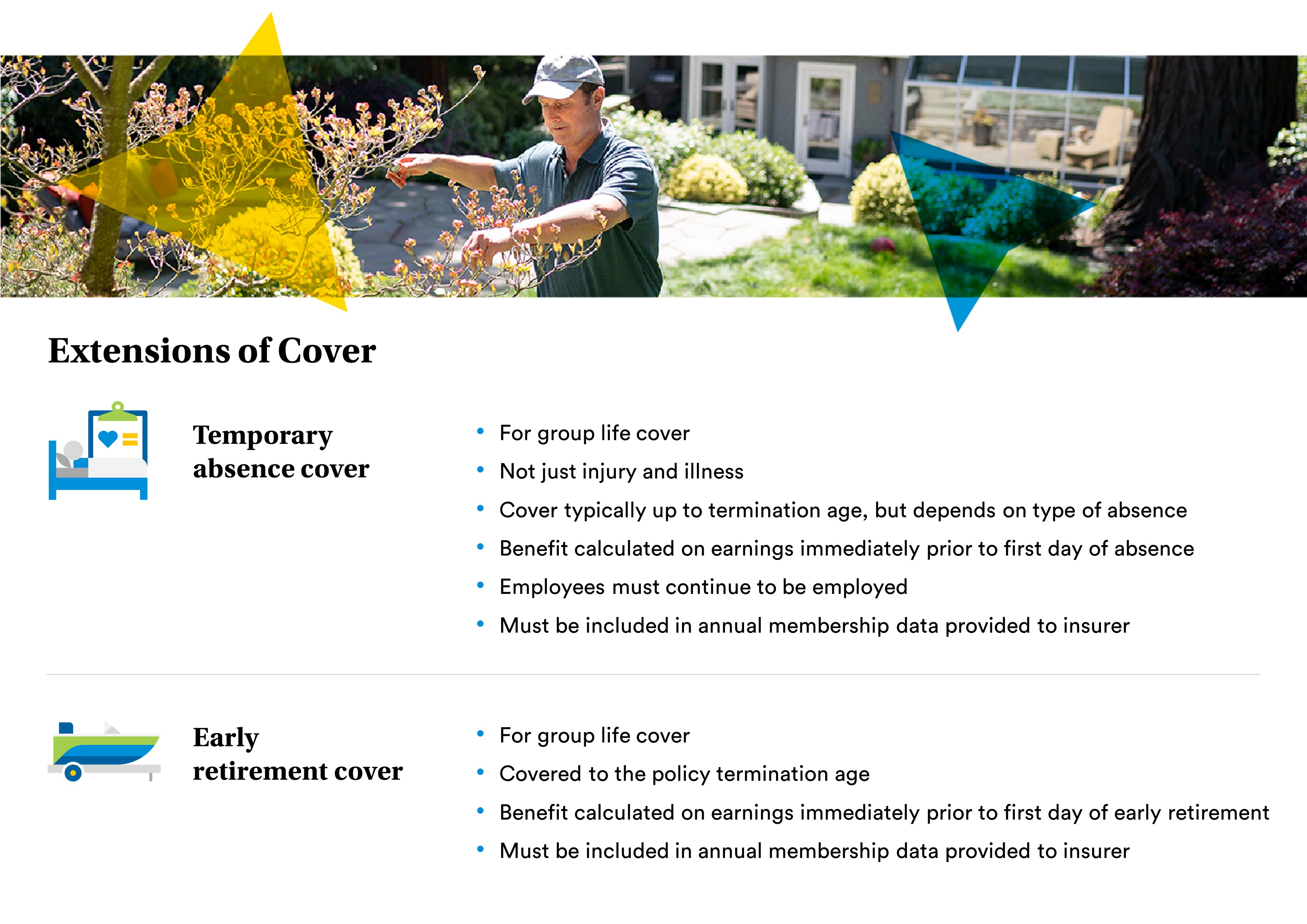

Available on group life insurance, this ensures cover continues if a member is temporarily absent from work due to illness or injury or other reasons such as maternity or paternity leave, gardening leave or a sabbatical.

For absences due to illness or injury, it’s normal practice to continue cover up to the policy’s termination age, although there are shorter terms, especially on some older policies.

Where the absence is for another reason, cover is typically continued for up to 36 months. There is some flexibility around this though. For example, at MetLife we can offer cover for up to 10 years on a case-by-case basis.

Cover is based on the level of benefit calculated immediately prior to the first day of absence and can allow for general salary increases as well, up to a specified maximum.

For cover to continue, employers must also ensure that any absent members continue to be employed and are included in the membership data provided to their insurer every year.

A cover extension can be added to group life to accommodate members who want – or need if it’s due to ill-health – to take early retirement. This gives them the security of life cover at a point when it might be prohibitively expensive to arrange themselves.

Where this extension is added, early retirees will be covered up to the policy’s termination age. As with temporary absence cover, benefit is based on the level of benefit calculated immediately prior to the date of early retirement and the employer must include them within the annual membership data provided to their insurer.

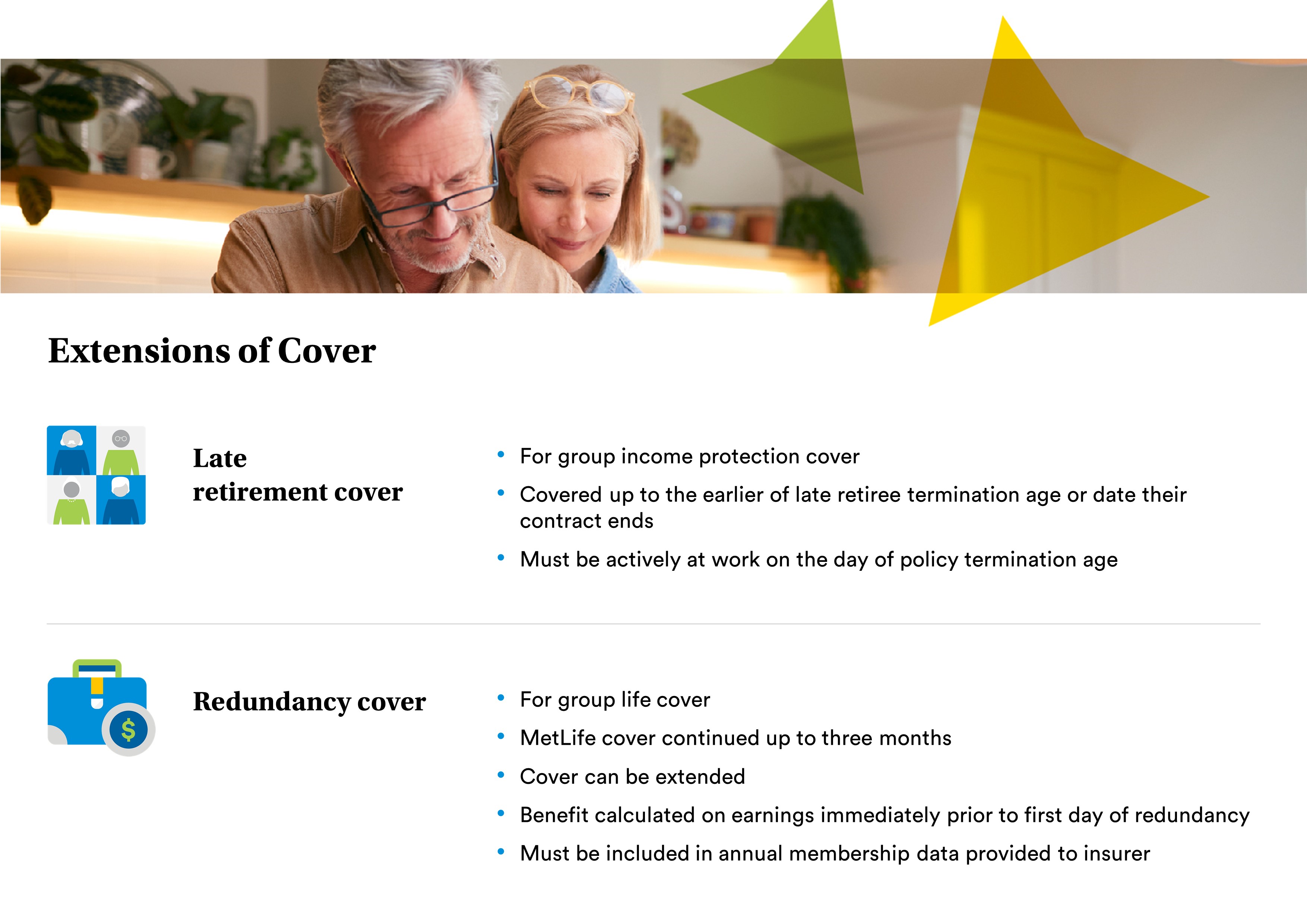

A late retirement option is available under group income protection cover, extending cover beyond the policy’s standard termination age for members who carry on working. They will be covered up to the earlier of the late retiree termination age or the date their employment contract or partnership ends.

The late retirement extension comes with an actively at work requirement. To benefit from the extension, the member must be actively at work on the day they reach the policy termination age. Anyone who is not actively at work at that point will not be eligible to extend cover until the late retiree termination age. For example, if a member says they have a particular condition, they can ask questions about the medication they’re taking, how long they’ve had it, how it’s changed over time and so on. This gives the insurer a much better picture of the member’s health and lifestyle.

Being made redundant can be a very unnerving time, with plenty of uncertainty around finances and what to do next. To give members the reassurance of cover during this time, insurers include redundancy cover on Group Life policies.

At MetLife we cover members for up to three months from the date of termination of employment at no additional cost, and it’s also possible to extend this if required.

Benefits are based on the member’s earnings, or benefit level, immediately prior to the date of redundancy and cover terminates at the earlier of the end of the extension, termination age or taking up paid employment.

As with the other extensions, the employer must include them within the annual membership data provided to their insurer until the redundancy cover extension ends.

These extensions help employers match cover to the needs of their employees, whether they’re taking time off for a new baby or an adoption, needing to work for longer, or unable to work due to an accident or sickness.

Insurer terms can vary across the market, so it is worth checking the detail of an insurer’s extensions thoroughly.. It’s also possible to alter the terms, such as increasing the length of cover for example. However, this will be determined on a case-by-case basis.