Technical

A quick guide to medical underwriting

Oct 07, 2022

Technical

Most employees can be offered cover under a Group Risk policy without needing to be medically underwritten. But, in a small number of cases, an insurer will ask an employee to provide medical information to better understand the risk.

This video explores why and how medical underwriting is undertaken and what the outcomes of the process may be.

When is medical underwriting undertaken?

There are three main situations where it may be necessary to medically underwrite a member. These are:

In each of these, the insurer is taking on more risk, so they want to be certain that it is priced accurately.

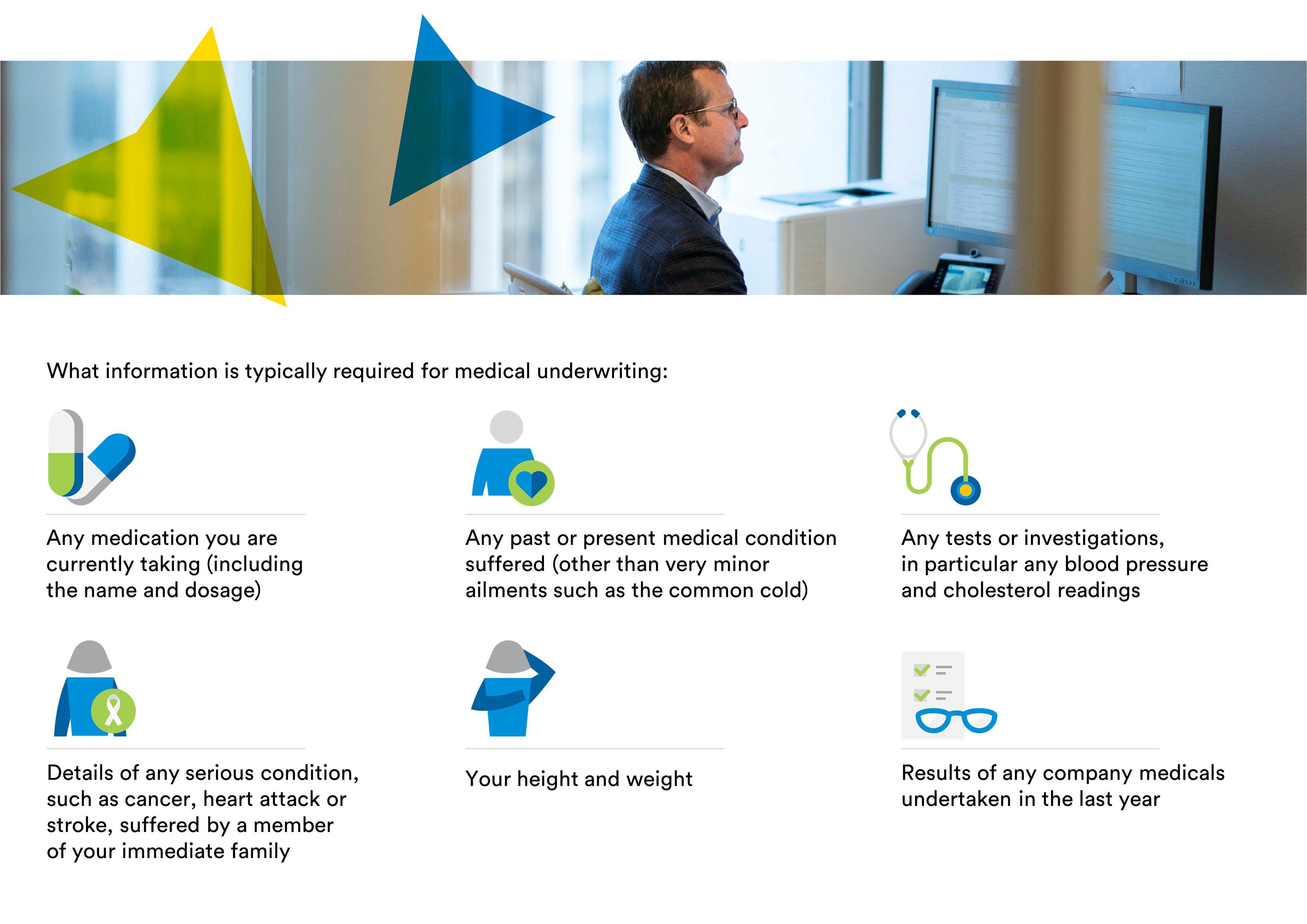

What medical information is required for medical undewriting?

To be able to medically underwrite a member, the insurer requires more information about their health and lifestyle. This includes:

Where medical underwriting is required, the insurer will contact the member directly to obtain the information.

At MetLife we offer members two options when it comes to providing this information.

Members can complete a health and lifestyle questionnaire themselves and return it by post or email.

We also offer tele-medical underwriting. With this, we arrange a telephone consultation for the member with a trained medical professional who will go through the questions with them. These consultations take at least 30 minutes and are arranged for a time that is convenient to the member, including evenings and Saturdays.

There are several advantages to tele-medical underwriting. As the consultation is with a medical professional, they will know when to ask additional questions to gain further insight.

For example, if a member says they have a particular condition, they can ask questions about the medication they’re taking, how long they’ve had it, how it’s changed over time and so on. This gives the insurer a much better picture of the member’s health and lifestyle.

Once a health and lifestyle questionnaire is completed, it is sent to the insurer’s medical underwriting team. Using their expertise, they are able to assess the risk and make a decision as to whether the member can be covered and if any conditions will apply.

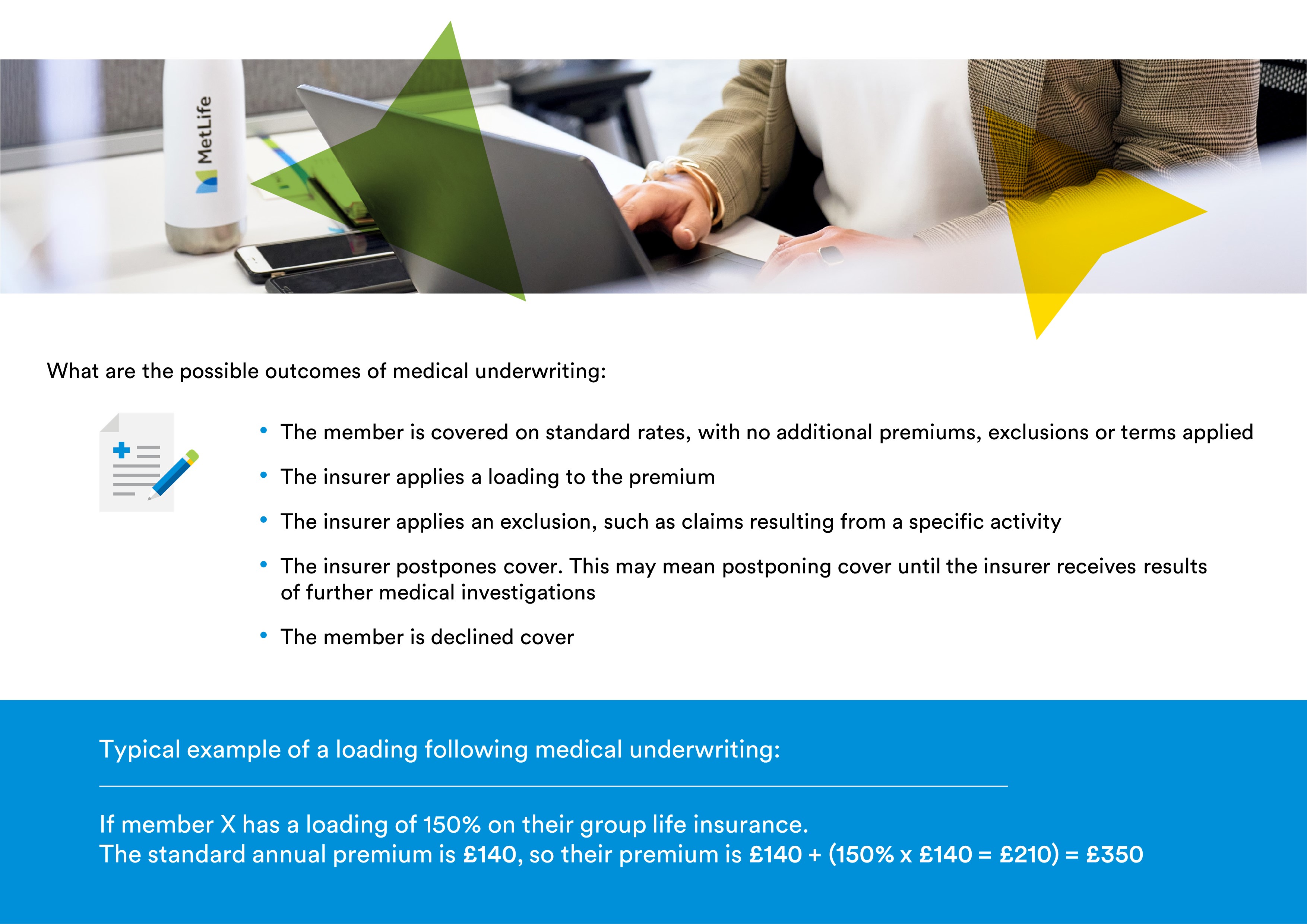

The best outcome is that the medical underwriting does not indicate any additional risk and the member is covered on standard rates, with no additional premiums, exclusions or terms applied.

Where the medical underwriting process finds that the member is a higher risk, the insurer could apply a loading to the premium. This loading, which typically runs from 50% to around 300%, is the percentage by which the premium is increased for that member.

For example, if member X has a loading of 150% on their group life insurance. The standard annual premium is £140, so their premium is £140 + (150% x £140 = £210) = £350.

Another option is to apply an exclusion. Member X is also partial to a spot of deep-sea diving in their spare time. As this is a hobby that can make group risk underwriters a little nervous, they might exclude any claims that result from this activity.

It’s also possible that the medical underwriters might postpone cover. This can happen where the member is undergoing medical investigations and the results are not yet known. This puts the cover on hold until more details are known to enable the insurer to make an underwriting decision.

In some instances, where the risk is very adverse, the member may be declined. For discretionary members, this unfortunately means they will not be covered at all, while for others, they will only have cover up to the free cover limit.

Medical underwriting can take time so the insurer will offer temporary cover while it is ongoing. This provides the member with the peace of mind that cover is in place if they did become unwell or die during the underwriting process.

To protect the insurer, a pre-existing condition exclusion is applied to this temporary cover. This excludes any claims that are the result of an existing condition from the last 5 years (for example). This does not need to have been diagnosed.

Temporary cover is usually in place for 90 days but it can be extended if an underwriting decision is still pending.

This depends. A forward underwriting bar may be applied at the point of underwriting. This grants some additional benefit to cover future increases, but a member may need to be medically underwritten again, depending on the terms.

For example, one insurer might offer a further 30% of benefit; another may apply the forward underwriting bar for two years, providing there are no benefit increases in excess of £100,000. If the member exceeds these terms, or a time period ends, they will need to be re-underwritten.

Another option is ‘OneStep’ underwriting where, providing there are no changes to the cover, members do not need to be underwritten again. At MetLife we offer this for policies of 20 members or more.

A one step underwriting bar of £5m is applied and providing the scheme doesn’t change cover and the member doesn’t exceed the £5m benefit increase, which is very unlikely, then there is no need for further medical underwriting.