Risk

Occupation and location risk factors for employee benefits

Mar 20, 2020

Risk

Where someone works and what they do can affect the level of risk on group risk policies. Integrating information on each member’s occupation and location into the quotation process helps to create an appropriate price for each risk.

This video explores how occupation and location factors affect insurance premium

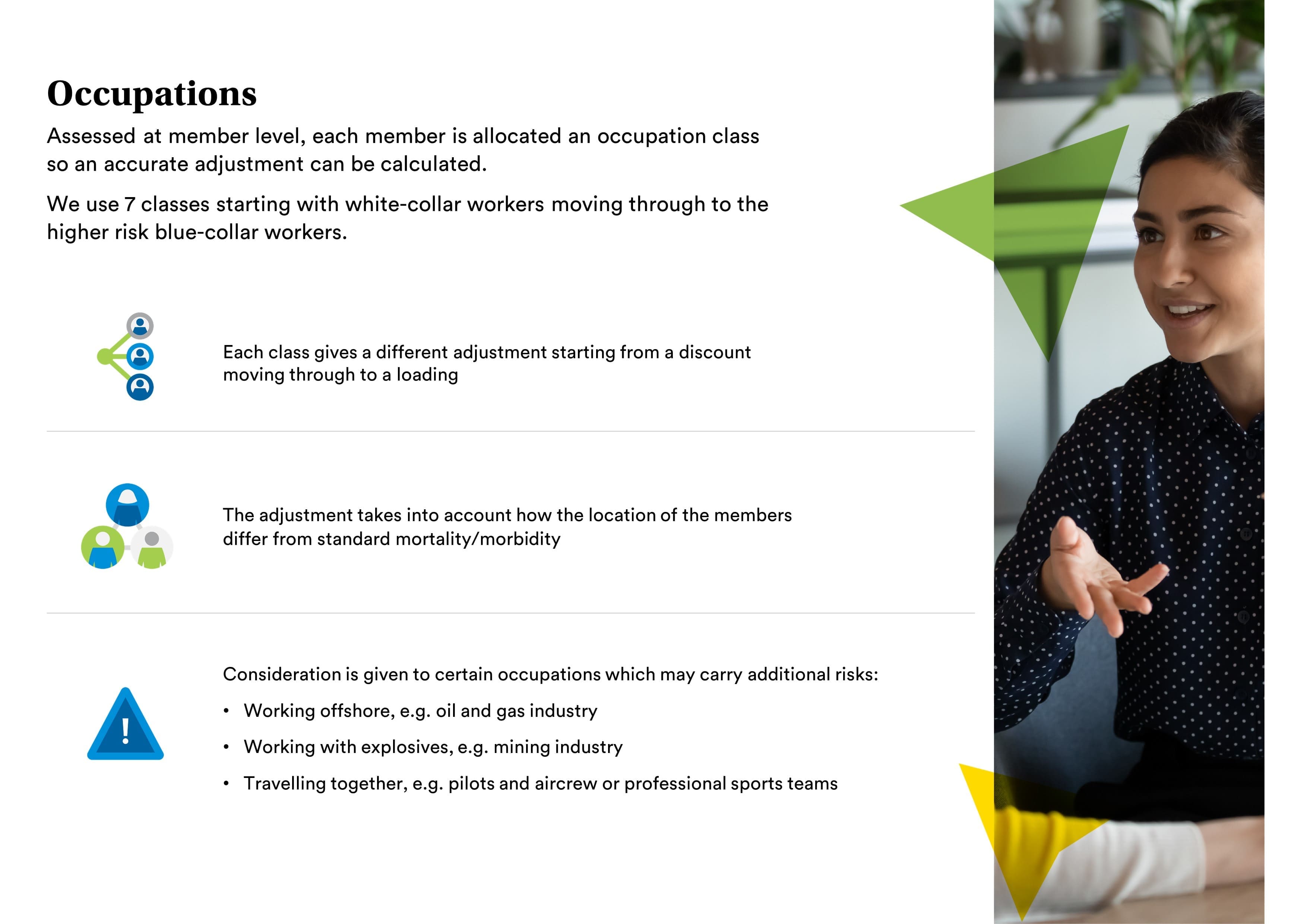

For occupation, a group risk insurer assesses how the job someone does affects their health and lifestyle, giving an occupational class to every member based on how their work affects risk.

Although occupational classes vary between insurers, depending on their view of risk, the following examples give an indication of the health and lifestyle factors that insurers take into consideration when setting occupational classes.

A director of a bank would be considered low risk. They’re white-collar, with their role largely desk-based and unlikely to put much physical strain on them.

They’re also well-paid, which means they’re more likely to enjoy an affluent lifestyle and have access to benefits such as private medical insurance to enable them to get any health issues looked at quickly.

An employee working on a production line in a factory would usually be considered higher risk.

Their job, and the environment they work in, could affect both their physical and mental health. It can often be a low paid role too, which can affect their lifestyle.

They are also less likely to have access to private medical insurance and may face difficulties taking time off to attend doctors’ appointments.

Once an insurer has this information, they can determine how each member’s occupation affects the risk across the scheme.

For group life, insurers look at how it affects mortality. The nature of some jobs will increase this risk. For example, someone working on an oil rig, where they might be in stressful and dangerous environments, faces a higher risk of dying than someone sat behind a desk on the mainland.

There is also a higher risk among lower paid members. They are less likely to lead a healthy lifestyle or be able to access private health screening and treatment.

On group income protection, there are two different elements to take into consideration.

The risk that a member will be unable to work due to long-term illness or injury but also the probability of getting them back to work.

As an example, reasonable adjustments can make it easy for someone who uses a wheelchair after a spinal cord injury to return to a desk-based job. But, if they were a bricklayer working on a construction site, returning to that job would be more challenging.

For both products, the occupation details for each member are accumulated to give an average for the group, which is then factored into the rate.

Location is another factor that can affect risk on both group life and group income protection. Where someone works will affect a variety of health and lifestyle related risks, especially as their work location is usually close to where they live too.

To illustrate this, compare the home counties with the Hebrides. The home counties are one of the more affluent parts of the country, with easy access to everything from education and healthcare.

In contrast, someone working in the Hebrides might have to travel to the mainland to access medical treatment. In an emergency, this could affect their chances of receiving treatment.

Diet and lifestyle vary around the country too, which can also affect the mortality and morbidity risks.

The value that insurers place on location could change in the future. As more people are working from home or in a hybrid manner since the pandemic, the location of the workplace may become less of an influence on risk.

Where it was common to live within commuting distance of the workplace, this is no longer a necessity and workforces are spreading across the UK and beyond.

At MetLife, we will continue to monitor this trend to ensure we accurately reflect location risk in our underwriting and pricing.